Trade finance moves billions of dollars through global supply chains every year. But buried within that scale is a silent problem: the same invoice or shipment can be financed twice by different lenders. When lenders cannot see each other’s positions, detecting this fraud is nearly impossible. The risk compounds across networks where visibility is fragmented, trust is limited, and reconciliation is manual. This is not a new problem, but it is one that validation registries, powered by registry logic and privacy-preserving techniques, are beginning to solve at scale.

Unlike more ambitious blockchain projects in trade finance that attempt to replace existing infrastructure, validation registries take a different approach. They sit alongside the existing banking ecosystem, allowing institutions to check whether an asset has already been financed without exposing competitors’ data or requiring a wholesale shift in how banks work. This is a practical pattern: a registry holds fingerprints or hashes of financed documents, not the documents themselves. Banks query the registry before approving new credit, and the registry confirms whether a match exists. No documents shared. No big new platform required. Just integration via existing networks like SWIFT (Society for Worldwide Interbank Financial Telecommunication).

In an episode of On The Block, Espeo Software’s YouTube series on blockchain and decentralised technology, we explore the mechanics of validation registries, how they sit within trade finance workflows, and why their modest, modular design is more likely to achieve adoption than grand platform plays.

What is duplicate financing and why it matters

Duplicate financing occurs when a single trade asset (an invoice, bill of lading, or shipment) is used as collateral for credit from multiple lenders simultaneously. The exporter or buyer presents the same document to Bank A, Bank B, and Bank C, obtaining financing from all three. Each lender believes it holds exclusive claim to that asset. When the asset is liquidated, there is not enough value to satisfy all claims. The result is loss concentrated among banks that were unaware of each other’s exposure.

This is not a theoretical risk. Trade finance operates through networks where lenders do not have complete visibility into one another’s books. A buyer in Shanghai might finance an order with Bank A in Shanghai, Bank B in Singapore, and Bank C in Hong Kong. Without a shared registry or reconciliation mechanism, each bank operates under incomplete information. The buyer has an incentive to misrepresent: by securing financing from multiple sources, they access more capital than the asset genuinely supports. The fraud can persist until settlement, when discrepancies surface.

“One of the silent problems in trade finance is that the same invoice, or the same shipment, can be financed twice by different lenders. If lenders cannot see each other’s positions, this is hard to detect.”

– On The Block, Espeo Software

The scale of trade finance makes this problem significant. According to the International Chamber of Commerce, global trade finance flows exceed $5 trillion annually. Even if duplicate financing affects only a small percentage of transactions, the absolute dollar exposure is substantial. Individual banks may not feel the impact acutely (losses are typically written off), but the system-wide cost is real: it manifests as higher interest rates, stricter collateral requirements, and reduced availability of trade credit in emerging markets where trust is lower.

Where duplicate financing surfaces in modern trade finance

Duplicate financing is most common in high-growth or high-risk markets where: – Multiple banks compete for the same clients and offer similar products without strong integration or visibility across competitors. – Documentation standards are loose, making it easy to present the same shipment or invoice in slightly different forms to different lenders. – Enforcement and legal recourse are weak, reducing the penalty for fraud. – Cash flow pressure is high, creating buyer incentive to seek financing from as many sources as possible. Specific trade finance products are more vulnerable than others. Open account financing, where the buyer is given extended payment terms by the seller, often sits outside formal registry or collateral tracking systems. Supply chain financing, where a fintech or bank finances inventory at multiple points in the chain, can create overlapping claims if the same goods are financed by both buyer and seller simultaneously.

Documentary credit (letters of credit) are less vulnerable because they are issued by a single advising bank and carry strong legal protections, but even here, fraud can occur when documents are counterfeited or a single shipment is presented to multiple issuing banks under false identities.

The validation registry pattern: what gets shared and what stays private

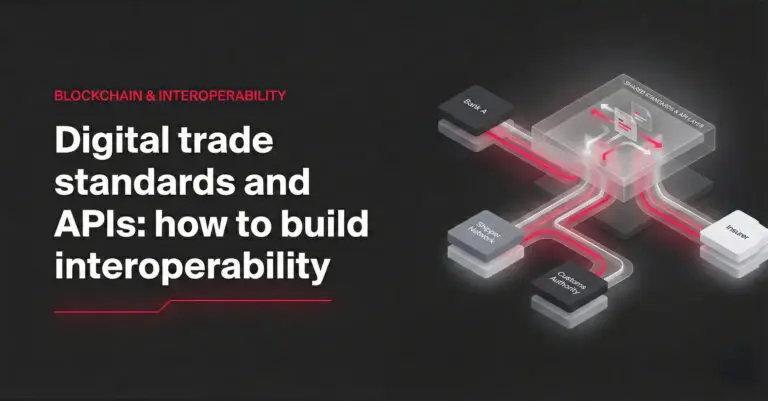

A validation registry operates on a simple principle: share the fingerprint, not the document. When a bank finances a shipment, it does not send the full invoice or bill of lading to the registry. Instead, it computes a cryptographic hash of the document and submits that hash plus minimal metadata (such as the exporter ID, shipment value, and financing date) to the registry.

This hash is a one-way function. It is computationally infeasible to reverse the hash back to the original document, and a tiny change in the document produces a completely different hash. The registry stores these hashes and metadata in a log. When a second bank is presented with the same document by the same exporter, it computes the hash and queries the registry. If the hash exists, the registry returns a match without revealing who financed it first, when, or for how much. If no match exists, the bank can proceed with confidence.

“Banks can check new financing requests against this registry. They don’t see competitors’ data, but they can see if something has been financed elsewhere.”

– On The Block, Espeo Software

Finances shipment

MD5(invoice) = abc123…

Store hash + metadata

Hash match? Yes / No

The metadata stored alongside the hash is intentionally minimal. A registry might store the hash, the exporter identifier (such as a tax ID or company registration number), the shipment value range (not exact value), the financing date (not time), and the asset type (invoice, bill of lading, etc.). This allows pattern-matching without exposing sensitive business intelligence. A competing bank cannot infer the lending terms, interest rate, or broader relationship with the exporter.

Different registry implementations vary in their approach. Some registries use a single standardized hash algorithm (such as SHA-256) applied to the entire document. Others allow banks to hash selected fields (such as exporter ID plus invoice amount) to accommodate different document formats. Some registries support probabilistic matching, which flags close matches even if the hash is not exact, for cases where document metadata might be slightly altered.

How validation fits into the workflow

Validation registries are not a replacement for due diligence; they are an additional layer of control within the existing approval process. The workflow typically unfolds as follows:

Exporter submits invoice or bill of lading to bank, requesting credit.

Bank computes hash and queries registry before committing credit.

Registry returns hit / no-hit. If hit, escalate or decline.

If no match, proceed with standard underwriting and approval.

On completion, financed asset hash is submitted to registry.

The registry check happens early, typically within minutes. It does not require human intervention in the common case (no match found). Most banks integrate the check via a simple API call: submit the hash, receive a boolean response, and continue. If a match is found, the bank can take action immediately – decline the request, request additional collateral, or escalate to a compliance team for manual review.

The critical detail is timing: the registry check must happen before the bank commits capital. If the check happens after credit is extended, it serves an audit function but provides no fraud prevention. Many early-stage trade finance blockchain projects made this mistake, building registries that confirmed what had already occurred rather than preventing fraud before it happened.

The API-first distribution model: why existing networks matter

A validation registry has no value without adoption. Early blockchain projects in trade finance attempted to solve this by building new platforms and asking banks to join. This requires each bank to integrate with a new system, learn new protocols, allocate budget, and accept governance by a consortium of competitors. The friction is high, and adoption is slow.

“This has already gone live through normal banking arrays. Banks can access such services via existing APIs and networks such as Swift. No need to join a big new platform. That’s a very different go-to-market model.”

– On The Block, Espeo Software

Validation registries that have achieved adoption take the opposite approach. Rather than asking banks to join a new network, they integrate with networks that banks already use. SWIFT (Society for Worldwide Interbank Financial Telecommunication), the messaging backbone of global banking, is the primary example. SWIFT operates standardized message formats and APIs that nearly all banks are already connected to. By embedding validation registry access through SWIFT APIs or SWIFT-compatible message formats, a registry becomes immediately accessible to thousands of banks without requiring new integrations.

This is a crucial insight for product design in trade finance. The go-to-market strategy should assume that banks will not change their core infrastructure to adopt a new product. Instead, the product should be designed to plug into infrastructure that already exists. This means compatibility with SWIFT, with existing correspondent banking networks, and with the APIs and message formats that banks already support.

Integration checklist for banks

For a bank or fintech evaluating whether to integrate a validation registry, the following checklist guides the decision:

- API availability: Does the registry offer an API compatible with your existing tech stack (REST, gRPC, message queues)?

- Integration scope: Which trade finance products does the registry support (open account, supply chain financing, invoicing, guarantees)?

- Hash algorithm: Does the registry use a standard hash (SHA-256, MD5) or proprietary method? Can your systems compute the required hash?

- Latency requirements: What is the API response time? Can it be called in real time during credit approval?

- Metadata submission: What metadata must you submit on each financed asset? Is this compatible with your systems?

- Dispute handling: How does the registry handle false positives (legitimate matches flagged as fraud) or false negatives?

- Audit trail: Does the registry provide logs of your own queries and submissions for compliance and reconciliation?

- Data retention: How long does the registry retain hashes? When are old records deleted or archived?

- Geographic coverage: Which countries and currencies does the registry cover? Does it support your primary trade corridors?

- Cost structure: Is the registry free, transaction-based, or subscription-based? What are the per-query costs?

Governance and dispute handling

A validation registry is only effective if the institutions that contribute to it trust both the governance model and the technical implementation. Poor governance undermines adoption even if the technology is sound.

Governance questions that must be resolved:

Who operates the registry? Possible models include a central bank (government-operated), a consortium of large banks (member-operated), a standards body (neutral third party), or a private company (for-profit). Each has trade-offs. A central bank may have enforcement power but be slower to innovate. A consortium may be faster but face conflicts of interest. A standards body may be neutral but lack operational resources. A private operator may be efficient but raise questions about data custody and incentives.

How are disputes handled? What happens when Bank A claims that a document financed by Bank B is fraudulent, or when a legitimate exporter is flagged as having duplicate financing due to a hash collision or data error? The registry must have a process to investigate, correct records, and provide recourse. This requires human review, which limits the ability to scale purely through automation.

Who controls access? Should all banks have equal access to query the registry, or should some institutions (such as central banks) have broader visibility? Should an exporter have the right to see which of its documents are registered, and to request deletion? These questions touch on privacy, competition, and regulatory compliance.

“Governance beats technology. Who controls the network matters as much as what runs under the hood.”

– On The Block, Espeo Software

In practice, most validation registries that have achieved adoption have chosen a hybrid model: a private or semi-private operator manages the technical infrastructure, but a consortium of banks or a regulatory body defines policy and handles disputes. This balances operational efficiency with stakeholder trust.

Beyond duplicate financing: the broader registry ecosystem

Validation registries were initially designed to detect duplicate financing, but the same pattern applies to other risks in trade finance. Registries are being built to flag fraud, track shipped goods, verify authenticity of documents, and reconcile settlements. Each registry may be operated by different entities, use different technologies, and serve different use cases. But they share the same principle: a shared truth maintained through distributed participation, without requiring participants to merge into a single platform.

“Projects that work either give everyone a clear benefit or they are backed by a regulation that simply forces the industry forward.”

– On The Block, Espeo Software

Looking ahead, the future of blockchain in trade finance is likely to be not a single network but a network of networks. Some registries will focus on documents (title, ownership, authenticity). Some will focus on fraud and risk (duplicate financing, counterfeiting, sanctions screening). Some will focus on payments and settlements (clearing across borders, currency conversion). These registries will be interoperable through standardized APIs and data formats, allowing a bank to query multiple registries in a single workflow.

“We will see a network of networks. Some will focus on documents, some will focus on fraud and risk, some will focus on payments and settlements. And they will talk to each other through standards and APIs.”

– On The Block, Espeo Software

How to start narrow and prove value

For banks or fintechs considering how to approach blockchain investment in trade finance, the guidance from industry practitioners is clear: start small and focused.

“If I were to suggest how to approach building a blockchain product for trade finance, I’d start with just one painful document or risk.”

– On The Block, Espeo Software

Rather than attempting to build a comprehensive platform that handles all trade finance risks and documents, successful projects typically focus on a single pain point. For duplicate financing, that pain point is clear: the cost of fraud and the friction of manual verification. A validation registry that eliminates that friction, without requiring institutional change, can achieve adoption quickly.

The approach is:

- Identify the pain. Which specific risk or document type causes the most frequent loss or operational friction?

- Measure the baseline. How much do duplicate financing, document fraud, or reconciliation delays cost today? Get numbers from your pilot banks.

- Design for integration. Build an API that plugs into existing systems. Use standard message formats. Minimize integration effort.

- Start with one corridor. Launch with a single country pair or trade corridor where the pain is highest and trust is lowest. Prove value before expanding.

- Iterate on governance. Get early feedback from participants on who should operate the registry, how disputes should be handled, and what metadata should be captured.

- Expand through standards. Once the core service is working, expand through standards and APIs rather than by building new platforms.

“Don’t wait for one magic platform. Instead, look for focused tools that can plug into the systems you already have.”

– On The Block, Espeo Software

This model explains why validation registries have achieved adoption more readily than other blockchain projects in trade finance. They solve a specific problem, integrate with existing infrastructure, and do not require institutional restructuring. They work because they are designed for the world as it exists, not the world as blockchain idealists might wish it to be.

Frequently Asked Questions

Duplicate financing occurs when a single trade asset (invoice, bill of lading, or shipment) is used as collateral for credit from multiple lenders without their knowledge. The exporter presents the same document to multiple banks and obtains financing from all of them. When the asset is liquidated, there is insufficient value to satisfy all claims, resulting in losses concentrated among lenders who were unaware of each other’s exposure.

Validation registries use cryptographic hashes instead of full documents. When a bank finances an asset, it computes a hash of the document and submits that hash plus minimal metadata to the registry. When another bank receives the same document, it computes the hash and queries the registry. If the hash matches, the registry signals that the asset has been financed elsewhere, without revealing which bank financed it or the terms.

SWIFT (Society for Worldwide Interbank Financial Telecommunication) has integrated validation registry services into its existing API infrastructure, making such services accessible to thousands of banks through familiar channels. By embedding validation registry access within SWIFT APIs rather than requiring banks to join new platforms, these services have achieved rapid adoption among financial institutions globally.

The registry check must happen early in the approval process, before the bank commits capital. The typical sequence is: financing request received, registry hash query initiated, registry returns match / no-match, and only if no match is found does the bank proceed with standard underwriting and approval. A registry check that happens after credit is extended serves audit purposes but provides no fraud prevention.

Banks submit a cryptographic hash of the financed document plus minimal metadata, typically including the exporter identifier (tax ID, company registration), shipment value range (not exact amount), financing date, and asset type (invoice, bill of lading, guarantee). This metadata allows pattern matching for duplicate detection without exposing sensitive business terms or competitive information.

Validation registries require a dispute resolution process to handle false positives (legitimate matches flagged as fraud) and data errors. This typically involves escalation to a human reviewer, who investigates the documents, contacts the participating banks, and corrects registry records if needed. Most registries maintain an audit trail of queries and submissions for compliance and reconciliation purposes.

Further Reading and Resources

- SWIFT – The global messaging network for financial institutions and primary channel through which validation registry services are accessed by banks.

- International Chamber of Commerce (ICC) – Develops standards for trade finance documents including UCP 600 (documentary credit) and covers trade finance risk and fraud patterns globally.

- Bank for International Settlements (BIS) – Publishes research and statistics on trade finance flows, risks, and systemic challenges in global banking.

- MonetaGo – Provides trade finance validation and supply chain financing platforms that integrate with existing bank systems via APIs.

- Securities Industry and Financial Markets Association (SIFMA) – Publishes guidance on trade finance best practices, fraud prevention, and regulatory compliance.

This post is based on an episode of On The Block, Espeo Software’s series on blockchain and decentralised technology. Direct quotes have been lightly edited for readability.